In case you missed it, my awesome husband Alex is doing a two-part series guest post answering the question of how we travel so much. Last week’s installment detailed points and miles programs and how to use them to your advantage. This week, he clears up some common misconceptions about credit cards and explains how using credit cards to maximize points and miles has actually improved his credit score! Thank you Alex and I hope you all enjoy! As always, feel free to contact me through the comments if you have any questions.

First, try to forget the commonplace wisdom that credit cards are evil. They aren’t. When used responsibly they help to build a sound credit report, and assist in raising your credit score. I should probably start off by stating two facts about the dangers of credit cards.

- Having several credit cards is only a bad thing if you depend on them to get by.

- Carrying a balance on any credit card at any time is very dumb; it will eventually cause your financial ruin.

Getting those two things out of the way first, now it’s time to explain how wonderful airline/hotel miles/points and using credit cards to get those miles/points can be for travelling practically for free!

When I started this endeavor, I had 0 credit cards and a terrible credit score. This is because no bank wants to give someone credit if they haven’t had credit before. Makes sense, they don’t know if they can trust you with large sums of money that you will borrow and pay back (aka using a credit card).

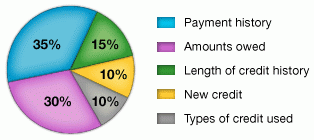

So I took my terrible credit score and got my first credit card at the age of 25 (embarrassing, I know). And after a few months of using the card and paying off my balance in full each month, my credit score went up a few points. It was still a bad score, but incrementally higher than before. I then started applying for a second and then later a third credit card, which (counter-intuitively) raised my credit score, thus allowing me to get even more credit cards. The chart below explains why this happens.

How your credit score is determined:

When you don’t use credit cards (or have any sort of credit in your name), your credit score is nonexistent in all of the categories. A huge portion of your credit score is made of up “Do you pay your bills on time?” (which we ALWAYS do) and “How dependent are you on this credit?” (meaning what is the debt-to-credit ratio I am carrying?). The more credit cards I have translates to a better credit score. I don’t use my credit cards to make any purchases that I cannot pay off at the end of the month; I use them as I had used my debit card for years. Thus, I am now only utilizing ~1% of the credit that has been given to me.

This shows the banks that I am:

- Trustworthy and will always pay my bills on time.

- I am not depending on the credit I have been given.

Having these two qualities means they are willing to give me even more credit. And so goes the cycle that has given me an excellent credit score now. Having an excellent credit score also helped Crystal and I qualify for a great mortgage rate for our house.

So now on to your questions:

Do you have a bunch of credit cards? Yes I do. They have helped me get an excellent credit score and travel the world for free.

Do you cancel them all the time? I occasionally have to cancel a card when the annual fee hits and the bank is not willing to waive the fee (which they sometimes do). Other times, they make a deal with me to pay the annual fee and keep the card, and they give me some sort of bonus in the form of miles/points. For example, the other day I called Chase because my British Airways card had a $75 fee come due. I said I wanted to cancel unless something could be done about the fee. They said “we can’t waive the fee, but if you spend $1,500 in the next 3 months, we will give you 9,000 Avios points.” I agreed to this. Here’s why: I can book a roundtrip ticket from Tally to Charlotte using 9,000 Avios. That ticket is valued at ~$300. I win.

How long do you have to keep them before you cancel them? This is tricky. After reading above, you saw in the chart that 15% of your credit score is determined by your length of credit history, so having a bunch of cards for 3 months would mess up your credit score. Keeping them for AT LEAST 1 year is a bare minimum, seeing as more often than not the first year fee is waived. Then when the annual fee hits, I do what I said in the previous answer while at the same time keeping my longest accounts open to increase the average age of accounts.

Now you know how we are able to travel so much without spending a lot of money on flights and lodging. Following Alex’s system has positively changed our lives and drastically increased the amount we are able to travel. I hope this two part series has been helpful and if you have questions, Alex and I are happy to work with you.

[…] resort (if you haven’t already, you can read about how we travel using points here and here). In a conversation with my mom about where to go, she mentioned that we might enjoy Arizona with […]

[…] travel. In fact, I have previously published articles about using points to travel (here and here) and we too prefer to travel in the shoulder season (both for budget reasons and to avoid crowds of […]